What is the issue and the short answer

The government has changed the tax law for taxing gains from debt mutual funds. So should you now invest in hybrid funds to save tax?

Earlier long term gains from debt mutual funds (held for more than 3 years) were taxed at 20%. Further, these gains were lower because acquisition cost was increased by inflation index . Under the revised law, the entire gain will be taxed at the tax rate applicable to you.

Assume you still want to invest in debt (also see Why you should invest in debt mutual funds). Does it now make sense to invest in debt mutual funds, if your tax bracket is 20% or higher? Is there a better alternative that has a better return after tax?

So then, should you invest in hybrid funds to save tax? The answer may be that the return after tax is only slightly better. However, the downsides may be higher. Let’s understand this.

Evaluation

What are hybrid funds

Hybrid funds are those that invest in both equity and debt and are classified by SEBI as hybrid funds. Here are the different types of hybrid funds and the long term capital gains tax treatment:

| Type of Hybrid Fund | Equity Investment | Type of Fund for tax purpose | Taxability of Long Term Gains |

| Conservative Hybrid Fund | 10% – 25% | Debt Fund | Same as normal debt funds, ie at tax rate applicable to you |

| Balanced Hybrid Fund | 40% – 60% | Debt Fund | As applicable to debt mutual funds, ie @ 20% with indexed cost |

| Aggressive Hybrid Funds | 65% – 80% | Equity Fund | As applicable to equity mutual funds, ie @ 10% |

| Equity Savings Funds (ESF) | 65% – 90% | Equity Fund | As applicable to equity mutual funds, ie @ 10% |

From the above, the Balanced Hybrid Fund seems like a good option, where it has substantial debt and the benefit of long term capital gains apply. However, there is very limited choice in this.

The other options are an Aggressive Hybrid Fund or an Equity Savings Fund (ESF), where the fund invests in debt and equity.

We have ignored Aggressive Hybrid Funds as they are riskier. In an ESF, the equity portion is split into equity and arbitrage on equity. Arbitrage takes advantage of the difference in current price of a stock and the price of that stock quoted for a future date. They take the opportunity offered by market inefficiency. Debt and arbitrage are the relatively safer portions of the fund.

Comparison with a combination of pure debt and equity funds

We did a quick calculation to see if ESF makes sense to buy as a part replacement for debt mutual funds.

Let’s assume that your debt:equity allocation is 50:50. Return on debt is 8% pa and on equity is 12% pa. The long term capital gains on equity is at 10% and you’re in the highest tax bracket at 30%. Let’s also assume that the ESF invests 20% in debt. Hence, if you were to invest Rs 10,000 each month for 5 years this is how it would be distributed:

Now let’s compare the returns after tax. In the first, the allocation is as above between Equity Savings Fund (50%), a debt fund (40%) and an equity fund (10%). In the second, it is pure debt fund (50%) and equity fund (50%):

Results

So the incremental return on investment is 0.47% over 5 years. The incremental return is higher if you stay invested for longer (1% for 10 years). The incremental return is lower if your tax rate is lower than 30%.

There are several downsides to the ESF. If you are investing in debt to provide constant income and a hedge against market downfall, then an ESF does not does not do this as well as a pure debt fund.

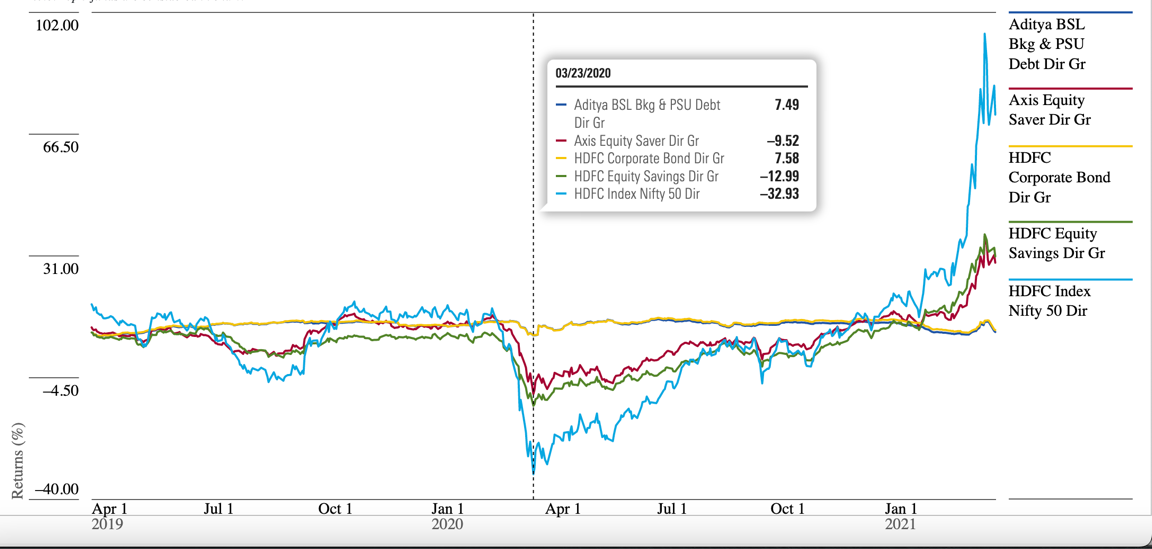

The following chart shows 1 year rolling returns for a period of three years, when the pandemic related lockdown hit:

(source: Morning Star Rolling Returns)

When the markets fell, any mutual fund that had more than 65% in Equity, had negative returns. ESF fell, but by less than half the fall of the Index Fund. However, debt mutual funds had a positive return. Hence debt mutual funds are a good hedge against market falls.

So, while ESFs are tax efficient, they will not provide a hedge against steep market falls.

Further, managing/balancing the desired debt:equity portfolio and diversification becomes difficult with such hybrid funds. Especially where a higher component of debt is required.

Such hybrid funds also have their own internal allocation to different types of equities and debt. That is unlike normal debt and equity funds that have the allocation based on their type. Hence this would require greater scrutiny and even then the allocations could change.

Hybrid funds also tend to have a higher Total Expense Ratio as compared with normal debt and equity funds.

Conclusion

So, if you are a short term investor and cannot afford to lose in a stock market downturn. You have no choice but to invest in debt mutual funds, despite no tax advantage for capital gains. (See our note on why debt mutual funds are better than bank fixed deposits)

If you are keen on maintaining a debt:equity ratio at higher than 30% for debt. Then a part allocation to ESF may get you slightly better returns. However, you’ll be partly giving up on how you would like your amounts allocated.

If your debt investment is 20% or less or you want the fund manager to decide the allocation based on market conditions, then go ahead and invest in hybrid funds.

All this until fund houses launch other innovative products.